Disruptive forces in healthcare, which healthcare leaders will need to address in their strategies if they intend to realize continued growth in the significantly changing marketplace.

Through extensive research into the thought-leading literature on the industry, as well as interviews with executives, physicians, policy makers and other stakeholders at the heart of the matter, Insigniam has distinguished ten disruptive forces in healthcare, which healthcare leaders will need to address in their strategies if they intend to realize continued growth in the significantly changing marketplace. These ten disruptive forces are outlined in the chart below.

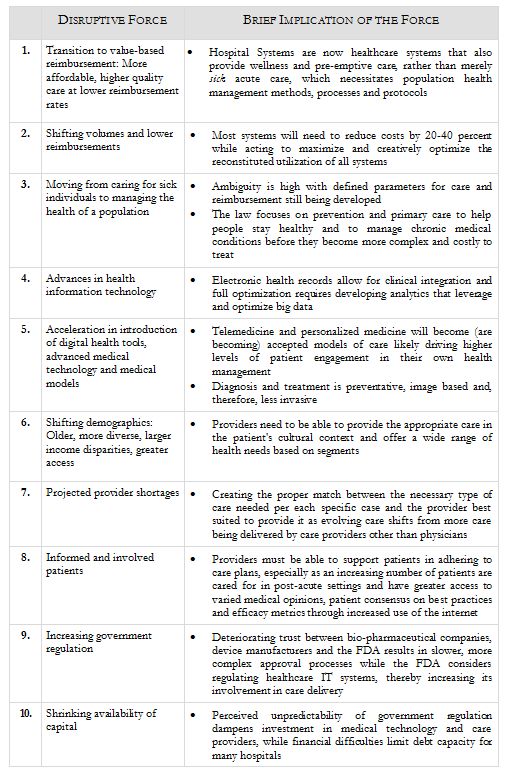

Each of these 10 forces creates significant implications for patients, providers and the healthcare industry, the most critical of which are listed below.

1. Transition to value-based reimbursement: Provide more affordable, higher quality care at lower reimbursement rates

- Higher quality and cost containment are now coupled

- Provider accountability for cost and quality of care

- Necessitates population health management methods, processes and protocols

- Evidence-driven care is required

- Transparency of cost, quality and community benefit data

- Must have integrated, aligned and engaged physicians

- Hospital systems are now healthcare systems that also provide wellness and pre-emptive care, rather than merely "sick" acute care

2. Shifting volumes and lower reimbursements

- Require most systems to take 20 to 40 percent of costs out of the system

- Must identify and remove non-value added cost

- Using scale to reduce costs and fixed expenses will lead to accelerating consolidation

- Maximize and optimize with creative and reconstituted utilization of assets from technology to facilities

- Develop a portfolio of facilities in the community from non-acute to acute that generates greater access at a lower cumulative cost and allows for treating patients at the lowest acuity possible

3. Moving from caring for sick individuals to managing the health of a population

- Insurers will be required under the Patient Protection and Affordable Care Act to completely cover such services as annual physicals, childhood vaccinations and dozens of screening tests

- The federal government is still defining the preventive care guidelines; ambiguity is still a challenge

- The law focuses on prevention and primary care to help people stay healthy and to manage chronic medical conditions before they become more complex and costly to treat

- New private health plans must cover and eliminate cost-sharing (co-payment, co-insurance, or deductible) for proven preventive measures such as immunizations and cancer screenings

- ePreventive measures for women went into effect in August 2012 with no cost-sharing

4. Advances in HIT

- Electronic health records allow for clinical integration

- Full optimization requires developing analytics that leverage and optimize big data

5. Acceleration in introduction of digital health tools, advanced medical technology and medical models

- Telemedicine, personalized medicine as accepted models

- Diagnosis and treatment is preventative, image based and therefore less invasive

- "Unconstrained connectivity" generated by providers and patients use of mobile devices

- Higher levels of patient engagement in their own health management

6. Shifting demographics: Older, more diverse, larger income disparities, greater access

- Providers need to be able to provide the appropriate care in the patient's cultural context

- Wide range of health needs based on segments

7. Projected provider shortages

- Make sure care providers are working to the full extent of their licensure

- Talent management for care providers

- Partnerships to stimulate (early) interest in these careers

- Evolving the care delivery system: more care delivered by other care providers other than doctors

- Creating the right match between the kind of care needed and the right provider to provide it

8. More informed and involved patients

- Shift from providing care to health management requires closer communication between pay providers, patients and care providers, especially before acute health care needs arise

- Providers will partner with patients to adhere to recommended care plans, especially as patients transition to post-acute care settings

- Consensus of best practices for developing patient engagement and efficacy metrics are lacking

9. Increasing government regulation

- Deteriorating trust between device and bio-pharmaceutical companies and the FDA, resulting in slower, more complex approval process

- FDA considering regulating healthcare IT systems, increasing its involvement in care delivery

10. Shrinking availability of capital

- Perceived unpredictability of government regulation dampening investment in medical technology and care providers

- Financial difficulties limiting debt capacity for many hospitals