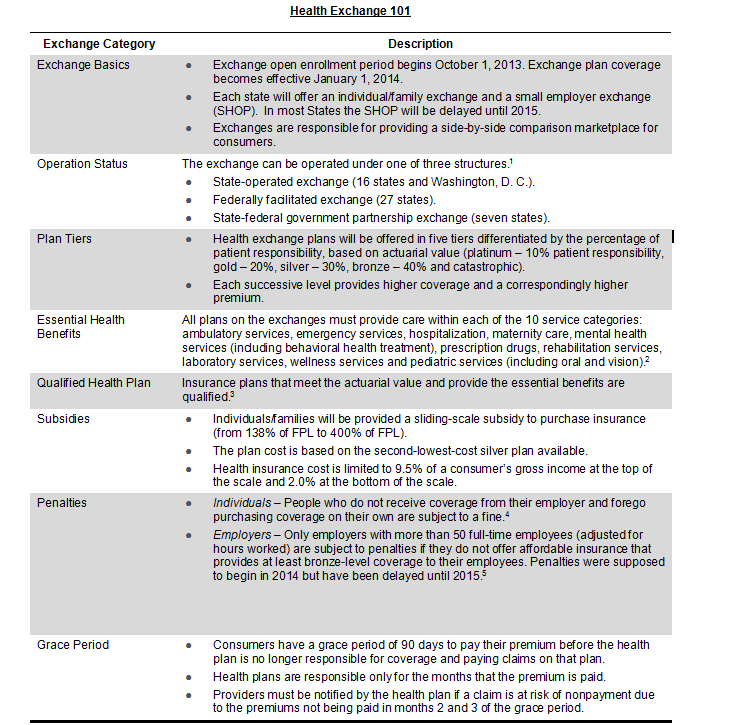

The Patient Protection and Affordable Care Act of 2010 created state-specific health insurance exchanges, now referred to as "marketplaces," that are designed to offer consumers a side-by-side comparison of available health plans. The goal of the marketplaces was to simplify the purchasing process for consumers to meet the federal individual mandate requiring insurance coverage.

Since the passing of the PPACA, the healthcare industry has learned that the legislation provides limited administrative guidance on an array of operational questions, which is resulting in a fair amount of confusion for individuals and businesses regarding their obligations and choices under the law. Also, there is a glaring lack of public awareness in many markets about exchanges and how consumers can access them starting in fall 2013.1 While the exchanges will first be made available to those primarily seeking individual coverage (outside of an employer), the exchanges will eventually open to small businesses.Starting in 2017, at the discretion of the individual States, large employers (100-plus employees) can access health exchanges, meaning that even more employers and employees will eventually be impacted.

Adding to the confusion, the federal government, earlier this year, announced a one-year delay of both the Small Business Health Options Program part of exchanges and the financial penalties for employers with 50 or more employees that do not offer health insurance.2 As a result, consumers and employers aren't the only ones confused about the exchanges. Healthcare providers are also unsure of how their business models, and ultimately, revenue will be impacted by the exchanges. How many individuals will enroll in plans offered on the marketplaces in 2014? 2015? Beyond? And, how will reimbursement rates compare to Medicare, Medicaid and existing PPO and HMO plans?

The next three years, 2014 to 2016, are likely to be a period of uncertainty, frustration and, ultimately, clarity as providers develop the proficiency to address the myriad challenges. Adminis-trators and legislators alike are hopeful that as educational campaigns roll out across the country, the level of awareness will improve and questions will be answered. Because of the market confusion, preparation by providers will be vital to minimizing patient disruptions and limiting negative financial impacts. Despite the open enrollment period beginning in October, there are a number of steps a provider can take to minimize confusion and improve operational efficiency.

How providers can prepare

Although some providers are negotiating contracts and modeling the potential implications of these contracts for marketplace plans, few organizations have thought through the operational realities of accepting new health exchange patients and payment rates on Jan.1, 2014. There are a number of areas that providers should evaluate to determine their readiness for exchanges, and these areas fit into three general categories:

● Operational processes

● Financial impact

● Education and outreach

Within each of these areas, a provider's readiness level and ability to address a given issue will depend on the organization's skills, the specific market conditions and the terms of the contracts in place. Providers should answer the following questions to assess their readiness.

Questions regarding operational processes

Is your organization out-of-network for the plans offered in your market's exchanges? Starting in January, hospitals and physicians will need to identify the exchange contracted and noncontracted health plans and health plan members. Many hospitals contract with all or a majority of the health plans in the market. Under exchanges, providers will have more non-contracted health plans and health plan products and may see more out-of-network patients. Admitting and registration staff will have to be educated as to whether or not these patients will be provided elective services or redirected to other contracted providers. Redirecting elective patients may be a big cultural and strategic change for some hospitals.

Have you outlined a process to accurately register exchange plan members? Do your contracts specify how exchange plan members will be identified? Capturing accurate and timely information at the time of registration will be a challenge for hospitals. It will be important for health plans to issue patient identification cards that specify individual product participation. The various plans may have a new fee schedule versus the current HMO or PPO fee schedule. Identifying and noting exchange plan coverage will be critical to supporting revenue cycle activities for proper rate and claim adjudication.

What is the patient's out-of-pocket liability? How much of patient out-of-pocket expenses can providers expect to collect from patients insured through the exchanges? Health plans are likely to limit patients' benefits on exchange products for elective services provided outside the network. Additionally, coverage levels may be lower than traditional PPO or HMO plans. As a result, patients will likely be responsible for higher out-of-pocket costs, and providers could be at greater financial risk (e.g, bad debt).

Questions regarding financial impact

What is the yield or margin related to the contracts for exchange-offered plans? Since the first year under health exchanges is expected to be bumpy, providers must be able to capture accurate payment information. Track your financial performance in order to determine if the exchange plan contracts need to be revised or terminated in the future. Evaluate how much of your business is actually derived from health exchange plans (will it be 1 percent, 2 percent or 10 percent of your net revenue?) and calculate the revenue impact of the agreed-upon rates in your contracts.

Are you prepared to track and monitor the exchange plans like your other contracts? Did the health exchange patient end up in the right insurance plan-code bucket? Health exchange plans are just like any other commercial product in a provider's contract portfolio. Therefore, patients need to be categorized by health plan and by product to ensure that you are accurately capturing the payments from both the health plan and the patient. Changes to revenue cycle practices may be necessary to make the patient's health insurance plan and product available as an insurance code at the time of registration. Few providers have considered establishing new insurance plan codes to ensure that patients are assigned to the correct health plan product (i.e., health exchanges).

Will your bad debt policies differ for these products? Will the increased revenue outweigh the bad debt losses? The amount of bad debt is another important financial metric to monitor. The additional coverage will undoubtedly improve revenue collection for many previously uninsured patients. But a larger patient obligation under the less expensive plans (i.e., the bronze plan 40 percent patient obligation and silver plan 30 percent patient obligation) is likely to increase bad debt.3

Is your state expanding Medicaid? Does your state offer a Basic Health Plan to help span the gap for people in the 75-200 percent of federal poverty level range? Eligibility for Medicaid will be an important issue to consider when developing strategies for patient access and building financial projections. For patients in between 75-200 percent of the federal poverty level, there are two issues.The first is whether or not patients at up to 138 percent of FPL will be covered by Medicaid, which will be determined by the state's decision on Medicaid expansion. Secondly, studies indicate that between one-third to one-half of patients with incomes in this range are likely to slip into or out of the range.4 The churning that results will create confusion regarding coverage for both patients and providers if patients change plans or go on and off Medicaid over a period of time.

Education and outreach

What steps is your organization taking to improve understanding about health exchanges in your community? Are consumers aware of the available plans and which plans you participate in? If consumers and businesses are confused, they will expect greater clarity from the hospitals and their physicians. Both hospitals and patients will need to understand what the patients' expected out-of-pocket costs are. Providers will need to educate frontline staff on the pertinent details of health exchanges, especially patient financial service personnel. Many providers are proactively conducting education sessions with community groups (e.g., parent teacher associations, town hall meetings, chambers of commerce) to clarify questions regarding signing up for coverage, subsidies and what they mean regarding access to care. Providers who are well educated about health exchanges can better serve their communities and ensure that consumers take full advantage of the new resource.

Conclusion

As the first major new federal healthcare program since the introduction of Medicare and Medicaid in 1965, health exchanges promise to bring plenty of strategic and operational challenges for even the savviest providers. Proactively addressing these challenges head-on will help any provider achieve success with exchanges in the new health reform era.

1 http://money.cnn.com/2013/04/23/news/economy/obamacare-subsidies/index.html.

2 Small business exchange delay source: http://www.nytimes.com/2013/04/02/us/politics/option-for-small-business-health-plan-delayed.html?_r=0. Large employer penalty source: http://www.nytimes.com/2013/07/03/us/politics/obama-administration-to-delay-health-law-requirement-until-2015.html?pagewanted=all.

3 Patient obligations are based on actuarial estimates for annual healthcare spend under the plan, as required by federal law.

4 Rick Curtis and Ed Neuschler, Income Volatility Creates Uncertainty about the State Fiscal Impact of a Basic Health Program (BHP) in California, Institute for Health Policy Solutions, with support from the California HealthCare Foundation, September 2, 2011.

5 Operation statistics as of July 2013.

6 https://www.healthcare.gov/glossary/essential-health-benefits.

7 https://www.healthcare.gov/glossary/qualified-health-plan.

8 http://kff.org/infographic/the-requirement-to-buy-coverage-under-the-affordable-care-act.

9 http://kff.org/infographic/employer-responsibility-under-the-affordable-care-act.